The ongoing Red Sea crisis continues to impact the shipping industry. The new transshipment networks set up to lower the impact of diversions in the Red Sea, have led to wider congestion at Mediterranean ports, such as Barcelona or Valencia. Large vessels sailing from the Far East are now offloading containers at western Mediterranean ports, while smaller ships then transport them to the final destinations at central/eastern Mediterranean ports.

Therefore, larger vessels can return immediately to the Far East rather than entering the Mediterranean Sea dead end caused by the Suez Canal diversions. Consequently, the rates on these trade lanes have increased. Further information is stated on the following pages.

LATEST DEVELOPMENTS

The Houthi militants continue targeting MSC vessels with the repeated assertion that they are “Israeli ships.” MSC vessels have been among the most frequently targeted ships by the militants and in a new statement from their spokesperson Yahya Saree they are claiming to have fired on three ships a total of four times without providing details or confirmation. (Source: Houthis Continue Targeting MSC Vessels Claiming Four New Attacks)

Yemen's Houthi rebels on 9 May claimed responsibility for two missile attacks in the Gulf of Aden on two Panama-flagged container ships that caused no damage. (Source: Yemen's Houthi rebels claim 2 attacks in Gulf of Aden)

According to recent data published by MSCHOA, the Maritime Security Centre Horn Of Africa, run by EUNAVFOR, the Houthis themselves have recently claimed they have attacked with more than 600 missiles and drones. MSCHOA’s count is 132 attacks in total, and even though a few vessels have been hit – and sadly also with loss of life as well as a sunk vessel – the amount of damage inflicted is modest compared to the number of attacks. However, from the perspective of reducing the risk of attacks from the Houthis, there has been no progress. As the data clearly shows, the number of attacks has been steadily increasing despite the military presence. (Source: Lars Jensen, Leading Expert in the Container Shipping Industry on LinkedIn)

Impact on Freight Rates

Container – Focus on the Mediterranean

The increasing transshipments activities via the Mediterranean have caused rate increases. The trade from Singapore (Asia’s largest transshipment hub) to Barcelona is a good example. According to Xeneta, the spot market freight rates jumped by 10% on this trade beginning of May to reach USD 4,394 per FEU. On 7 May, the average waiting time to berth at Barcelona increased to 3.53 days, and congestions is increasing further.

Also, the trade lane from Singapore to Las Palmas tells a similar story. Spot rates hit a Red Sea crisis peak of USD 6,217 per FEU in mid-January, but then fell back by 37% to USD 3,909 at the start of April. However, increasing port congestion meant this softening market did not last and rates began to increase sharply again, up by 38% to reach USD 5,448 per FEU on 5 May.

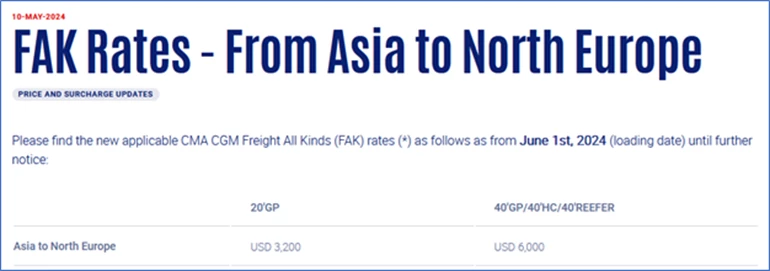

Shipping lines, such as CMA CGM, have started to announce GRIs starting from 1 June 2024 responding to the above demand vs. space gap:

This is an increase of approx. USD 1,000 compared to May 2024 rate levels. Other shipping lines will follow. At this stage, space and rate commitments on affected trade lanes are simply impossible, as shipping lines are not willing to commit to rate validities for longer than 1 month.

(Source: https://www.cma-cgm.com/news/4702/fak-rates-from-asia-to-north-europe).

Breakbulk (no changes since last report from 23.04.2024)

The ongoing disruption in the Red Sea continues to force multipurpose and heavy-lift (MPV/HL) carriers to sail longer routes to maintain their service schedules, modestly boosting rate-based MPV indices in April and May also.

Liner services have adapted to the market situation, as e.g. GMB Liner, who have suspended their service from Europe to Middle East due to a fall in demand, as steel products are sourced from elsewhere to cope with the current market constraints.

While the Red Sea situation remains volatile, we can expect carriers to take additional evasive action at any time.

Airfreight

Strong demand for e-commerce from the US and Europe that drove global air cargo volume growth in the first quarter is expected to lead into a “heavy” peak season later this year. However, the airfreight market is heading for a longer-term shortage of capacity and will struggle to accommodate the growing volume. (Source: Freight Forward: Rates on the Rise)

The capacity from Europe to Middle East is stable, but from Asia to Middle East we can see an increasing demand (as response to the constraints on ocean freight), which had led to rate increases for air cargo shipments ex Asia.

Shippers continue to turn to air cargo due to unreliability in ocean freight services. The market is experiencing a shift in transport mode, this time around the disruption has been caused by ongoing conflict in the Red Sea. Consequently, air cargo demand from Asia and the Middle East to Europe saw a substantial increase, leading to a significant month-on-month rise in air cargo rates in the affected region. Moreover, factors like the Qing Ming festival in China, Ramadan in Muslim countries and the Easter break has affected transshipments via the Middle East.

Also, other recent disruptions, including the floods in the UAE and Kazakhstan and the eruption of Mount Ruang in Indonesia, keep rising the overall interest in airfreight solutions.

SURCHARGES (no changes since last report from 23.04.2024)

Diversions away from the Suez Canal have hit ocean freight trades hard from Asia to the Mediterranean, North Europe, and US East Coast. However, it could be argued cargoes moving in the opposite direction on the backhauls have been hit even harder by these surcharges.

Effect – North Europe to Far East

Moving from USD 400 per FEU by the end of 2023 to more than USD 1,000 per FEU by mid-February, market average spot freight rates have gone up by 150% in six weeks.

Within these market average spot rates, some shippers have been paying upwards of USD 1,000 in additional costs while others have managed to avoid surcharges altogether, with an average of USD 591 per FEU.

Effect – Mediterranean to Far East

Surcharges are spread in the range of USD 400 (mid-low) and USD 1,100 (mid-high) per FEU, with an average of USD 639.

Effect – North Europe to Australia and New Zealand

Shippers and BCOs are paying average surcharges of USD 854 per FEU within a total spot rate of USD 2,400 per FEU. This positions the trade slightly above a classic backhaul and slightly below a classic fronthaul in terms of the total spot rate and % of surcharges to overall cost.

Wide-ranging effects

The effects of the crisis are highly individual, and shippers, carriers, and freight forwarders are fighting as hard as they can and entering negotiations with the single aim of reducing the effect of the crisis on their business as much as possible – whether that is through surcharges or service reliability.

Surcharges are more significant on long-term rates

For a standard FEU, the Red Sea surcharge for exports out of the Mediterranean on long term contracts sits higher than North European exports, with a spread of USD 162. However, while the market low for both trades sits at USD 400, the market high sits at USD 1,295 for the Mediterranean and USD 750 for North Europe. Bringing a reefer out of North Europe heading for Far East, the average surcharge sits at USD 1,007 per box.

IMPACTS ON SCHEDULE RELIABILITY (no changes since last report from 23.04.2024)

The schedule reliability on the North Europe to UAE Main corridor has decreased by 51.57% compared to November 2023. CMA CGM is the most reliable carrier (33.33%) while Maersk is the least reliable (12.73%). The green line below shows the massive drop in reliability in February, which is now flat lining again. (Source: xeneta.com).

OUTLOOK

We don’t see the Red Sea situation changing any time soon and the above-mentioned trends are likely to continue throughout H2 2024.

OUR ADVICE

This ongoing crisis will continue to impact rates and increase uncertainty within global supply chains. It is important to stay up to date, book well in advance and potentially look for alternatives, where available. Please contact us on time to discuss your transport inquiry.

We recommend that our customers try to build in a degree of flexibility in these times of uncertainty. We recognise that this is not straightforward and requires multi-party coordination. We should, where possible and reasonable, consider airfreight as alternative transport mode.

We are here by your side to keep your supply chains moving and help identify the most suitable and economic mode and route for your cargo transport. Contact your local Bertling office for further updates: https://www.bertling.com/offices/.

For air freight inquiries:

Janine Seemke

Global Head of Airfreight

P: +49 40 32335554M:+49 173 3893139

E: janine.seemke@bertling.com

For sea freight inquiries:

Samuel Semple

Group Pricing Manager – Ocean Freight (FL)

P: +49 40 3233550M:+49 1732069897

E: samuel.semple@bertling.com