Ocean freight container spot rates have risen sharply on the world’s top trades since the start of May, prompting speculation that the peak season has arrived early in 2024.

What is less clear are the reasons behind these dramatic rate movements.

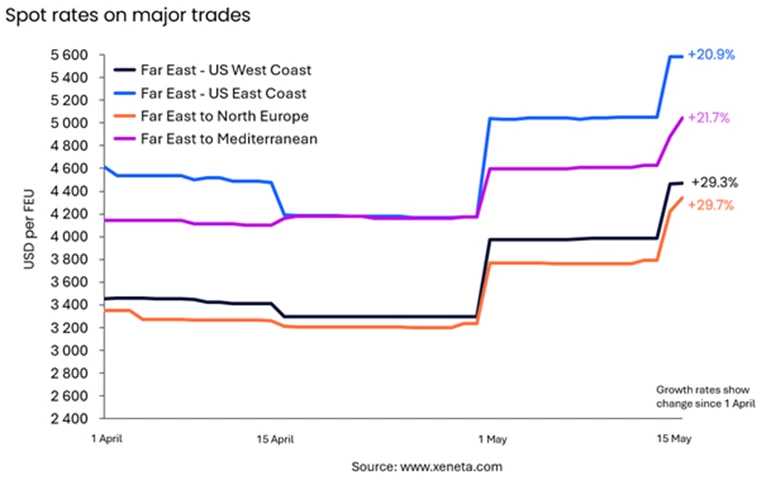

The biggest rise comes on the Far East to North Europe trade which increased by 30% from 1 April (USD 3 349) to stand at USD 4 343 per FEU on 16 May. This is 198% higher than 12 months ago (USD 1 456).

From the Far East into the US West Coast, rates have increased by 29% since the start of April (USD 3 456) to stand at USD 4 468 per FEU on 16 May. This is 214% higher than 12 months ago (USD 1 422).

From the Far East into the Mediterranean, rates have increased by 22% since 1 April (USD 4 144) to stand at USD 5 044 on 16 May - an increase of 100% compared to 12 months ago (USD 2 521).

From the Far East into the US East Coast, rates have increased by 21% since 1 April (USD 4 617) to stand at USD 5 584 on 16 May - an increase of 129% compared to 12 months ago (USD 2 434).

Emily Stausbøll, Xeneta Senior Shipping Analyst, said: “There are numerous reasons for these rate increases, and the speed at which it has happened has caused nervousness in the market.

“Demand reached record levels in Q1 2024, up by 9.2% compared to Q1 2023, and comes at a time when the Red Sea situation is putting increased pressure on shipping capacity.

“But significantly, this is all taking place while the chaos of port congestion and lack of available capacity during the Covid-19 pandemic is still fresh in the memory of shippers.

“Lessons will have been learned from the pandemic. If shippers fear there is going to be a squeeze on capacity during the peak season in Q3 then they are going to start importing more goods now.

“If these increased volumes need to be moved on the spot market then it is going to put upwards pressure on rates.

“Many US shippers used 2023 to bring down inventory levels from the pandemic highs, which means there is likely space in newbuilt warehouses to frontload imports ahead of peak season and build a buffer into supply chains. The risk of having too high inventories is more palatable than the risk of having goods arrive too late.”

Long term rates on major trades have remained relatively flat in Q2 and not followed the short term rates, which suggests carriers are playing the two markets separately.

Stausbøll said: “Carriers have now mostly agreed new long term contracts for the next 12 months at lower rates than they maybe could have pushed for given the spot market is still elevated.

“This was likely done to secure long term volumes due to the prospect of a large-scale return of container ships to the Red Sea, a situation which is currently absorbing some of the overcapacity in the market.

“If carriers are able to make money from shippers who want to use the spot market to frontload additional volumes ahead of peak season, then clearly they are going to take that opportunity and that is what we have seen in the rate increases in May.

“Shippers will also be aware that the bigger the gap gets between the short and long term markets, the higher the risk becomes that their cargo may get rolled, especially if it is being moved on a long term contract at the low end of the market. Even if there is still capacity in the market, the fear factor can push up rates.”

The shadow of black swan events also looms large over the industry. As well as the Red Sea crisis, there are still ongoing restrictions in the Panama Canal and signs of escalation in the US-China trade war.

Stausbøll said: “Who can be confident in saying there isn’t going to be another black swan event in 2024?

“This week we have seen the announcement of new US tariffs on imports from China, there are fears over port congestion in the Mediterranean and Far East, there are fears over equipment shortages, and there is the threat posed by labor negotiations on the US East Coast which has the potential to cause massive disruption.

“If shippers have the ability to build up inventories just in case these threats become a reality then it is not surprising they are doing so.”

Stausbøll reiterated that, while spot rates are increasing on major trades out of the Far East, it is vital for shippers to understand their individual supply chains and the risks attached to them, in order to make them more resilient.

She said: “We are seeing dramatic increases on trades out of the Far East, but the backhauls remain flat.

“There is also little movement on the North Europe to US East Coast trade which has seen average spot rates decrease by 3.3% since 1 April.

“Each shipper will also have different tolerance levels to risk. Some may be willing to pay more to secure additional volumes on the spot market ahead of peak season, while others may be happy to rely solely on their long term contracts.

“There is no single ‘best solution’ in such a complex market - it is a case of each shipper understanding their own supply chains, assessing the risks and using data to gain insights and make evidence-based decisions.”